How Stablecoins Are Changing Fintech Infrastructure Today

Link to the full Research in PDF

Executive Summary:

The stablecoin market surpassed $300 billion in total capitalization in late 2025, representing a ~50% year-over-year increase. Annual settlement volume hit $33 trillion, eclipsing Visa's throughput. Stablecoin issuers now collectively hold more U.S. Treasuries than most sovereign nations. By some estimates the market could exceed $1 trillion in circulation by late 2026 and $2 trillion by 2028, driven by use cases far beyond digital asset trading: B2B settlement, remittances, e-commerce, treasury management, and payroll.

The Current Payment System: Overpriced & Inefficient:

Traditional payment rails rely on multiple intermediaries, driving up costs, slowing transfers, and instances of rejected payments. A typical cross-border transaction passes through a chain of correspondent banks, each extracting fees of 0.3% to 1.0%, before reaching its recipient, often three or more days after initiation. In aggregate, businesses and consumers absorb total fees of 1% to 3% on every international transfer, with settlement timelines spanning multiple business days.

Stablecoins are able to be transacted 24/7/365 with near 0 fees, which represents a significant upgrade to banking institutions, which are only open 23% of hours, slower, and much costlier. This category shift is currently ongoing across all of the fintech space with profound implications.

Thoughtful Regulation Implemented as a Catalyst:

The GENIUS Act, signed into law in July 2025 alongside its House companion the STABLE Act, established the first federal regulatory framework for payment stablecoins in the U.S., requiring one-to-one reserve backing and creating clear licensing pathways for issuers. Critically, the legislation clarifies that payment stablecoins are neither securities nor commodities, removing the regulatory ambiguity that kept institutional players sidelined. That legal clarity is the catalyst which gives banks, fintechs, and payment networks the confidence to build stablecoin products at scale, potentially unlocking trillions in flows.

Globally, in December 2024, the EU's Markets in Crypto-Assets regulation (MiCA) went live, establishing a single EU license that unlocks all 27 member markets via passporting, and institutes a 1:1 reserve requirement that builds issuer confidence. In Asia-Pacific, Hong Kong has emerged as the region's primary hub through stablecoin licensing and a regulatory sandbox that allows banks to test operations before launch.

Stablecoins as The Treasury Demand Engine:

Today, the US is running annual deficits approaching $2 trillion, and total debt of almost $39 trillion. The U.S. also has approximately $10 trillion in existing debt that is expected to roll over by the end of 2026. The traditional buyer base for U.S. debt securities has been consistently contracting for the last decade. In 2011, China and Japan alone held nearly 23% of the outstanding US Treasury debt. By late 2024 however, their combined share had collapsed to only 6%. The Federal Reserve, while simultaneously engaged in quantitative tightening, is no longer a consistent buyer either. As a result, The U.S. needs a new and reliable source of demand for its paper, and stablecoins have emerged to meet that need.

The current administration also agrees with this view as Treasury Secretary Scott Bessent has been a direct voice on this thesis. Speaking publicly in May 2025, he stated: "I've seen estimates that just over the short term, stablecoins could create $2 trillion of demand for US Treasuries and Treasury bills. Put that in context, the number is probably about $300 billion right now." Bessent further argued that "a thriving stablecoin ecosystem will drive demand from the private sector for US Treasuries, which back stablecoins. This newfound demand could lower government borrowing costs and help rein in the national debt." Both Scott Bessent and President Trump’s administration understand the significant opportunity that stablecoins bring to the U.S.

Dollar-backed stablecoins require reserves, and under the GENIUS Act signed by President Trump in July 2025, those reserves must be held in high-quality liquid assets, with short-term US Treasuries included. Every dollar of stablecoins issued is, in effect, a mandated buyer of US government debt. Bessent, speaking at the Treasury Market Conference in November 2025, noted that the stablecoin market, currently valued at around $300 billion, "could grow tenfold by the end of the decade thanks to the GENIUS Act."

The geopolitical dynamic is equally impactful as dollar-pegged stablecoins now represent over 99% of the total stablecoin market cap. Their growth also extends dollar-denominated financial access to hundreds of millions of people globally, generating additional global demand for U.S. securities. At the signing of the GENIUS Act, Bessent described the administration's plans in a single statement: "The dollar now has an internet-native payment rail that is fast, frictionless, and free of middlemen." Federal Reserve Governor Stephen Miran also reinforced this view, noting that "stablecoins are already increasing demand for US Treasury bills and other dollar-denominated assets by purchasers outside the United States, and that this demand will continue growing." The US government has structurally aligned its fiscal interests with the growth of the stablecoin sector, a clear catalyst for its growth.

Why Global Businesses Pick Stablecoins:

Global businesses require global currency rails, but banking relationships are difficult to earn and often entirely inaccessible to businesses operating in emerging markets. Traditional payment rails also introduce significant FX risk when exchanging between currencies. The cost of this complexity lands disproportionately on markets in LATAM and APAC that stand to benefit the most from access to North American capital markets infrastructure. Stablecoins resolve this at the protocol layer, removing the need for intermediaries on both ends.

Instant Settlement & Conversion: Settlement takes minutes, eliminating FX exposure across the settlement window. Global transactions become simple, bilateral, and near-instantaneous regardless of the currencies involved.

Direct Dollar Access: No banking or correspondent relationships required. Any business with a digital wallet can access dollar-denominated liquidity regardless of jurisdiction or credit history, opening commerce in markets previously locked out of global payment flows.

Programmable Compliance: KYC and AML rules can be embedded directly into the transaction logic, enabling autonomous treasury management without reliance on manual compliance workflows or third-parties.

Liquidity & Low-Cost Transfers: Stablecoin liquidity is available 24 hours a day and 365 days per year. Transfer fees for stablecoins are over 90% cheaper than traditional banking rails, making high-frequency and cross-border payments economically viable at scale for the first time.

The World Needs Digital Dollars:

For the majority of the world's population, the local currency is not a reliable store of value. Inflation rates across Latin America, Africa, and the Middle East, routinely outpace those in the US. In some cases, countries in these regions are running at double digit inflation rates or worse on a sustained basis. In these environments, holding local currency is a slow and predictable loss of purchasing power. The US dollar, by contrast, represents stability, global acceptance, and access to the world's largest financial system.

Until now, accessing and holding dollars required a bank account, a functioning financial institution, and in many cases, a government willing to allow it. Stablecoins remove all three barriers. An individual in Argentina, Nigeria, or Turkey, can hold dollar-denominated value with no bank, no intermediary, and no permission required. The global application of stablecoin technology represents billions of new potential users, who are choosing between a dollar in their pocket, and a local currency that erodes the moment that they receive it.

Accelerating Adoption & Tailwinds:

Stablecoin adoption is increasing at a rapid pace. Outstanding stablecoin supply has reached $307 billion, with a total annualized transaction volume of nearly $33 trillion in 2025. However, commercial payments represent only $390 billion of that total as the outstanding supply also grew 49% in just 2025 alone. Three major regulatory frameworks passed in the past twelve months have removed the primary structural barriers to institutional and commercial adoption.

Looking ahead, projected real-world stablecoin payments are expected to reach $600 billion in the next 2-3 years, with total payment flows projected to reach $56 trillion by 2030. Today, nearly 99% of the current transaction volumes are infrastructure movements, with real-world commercial payments accounting for only 1% of total transaction volume, indicating the commercial layer still remains in its earliest stages of development.

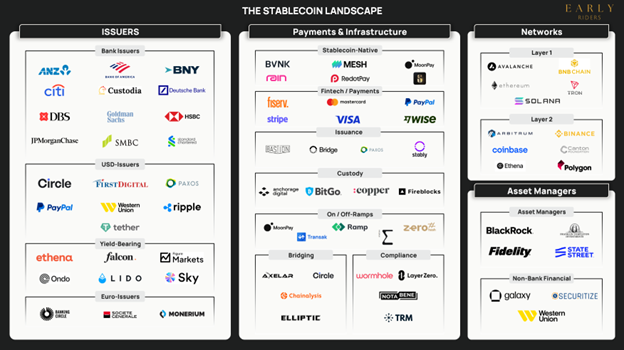

Fragmentation Represents an Opportunity:

USDC and USDT hold nearly 60% and 30% of the current market respectively, with the remainder split among a growing share of additional issuers. Following the passage of the GENIUS Act, major financial institutions, technology platforms, and sovereign entities are actively developing their own stablecoins. We anticipate that the connector rails that route payments between these issuers will capture the lion's share of value created in the space.

The market fragmentation challenge is currently multidimensional as liquidity is siloed across ten or more issuers with limited interoperability. Merchants and platforms must integrate each stablecoin separately, creating technical friction that limits payment acceptance. The same stablecoins exist across fifteen or more blockchain networks, fragmenting liquidity and requiring separate integrations for each. Moving between stablecoins requires multiple steps through exchanges adding cost, time, and counterparty risk. Businesses receiving payments in multiple stablecoins must manage separate wallets, reconciliation workflows, and conversion processes across each, which creates meaningful operational overhead.

This fragmentation operates across three distinct layers:

Issuer Fragmentation: USDC, USDT, PYUSD, bank-issued coins, and platform-native stablecoins each require separate integrations and carry different counterparty, compliance, and liquidity characteristics.

Chain Fragmentation: The same stablecoin exists across numerous networks like Ethereum, Solana, and a growing number of Layer 2 networks, which fragments liquidity pools and requires independent integrations for each.

Liquidity Fragmentation: Stablecoin liquidity is distributed unevenly across exchanges, payment processors, wallet networks, and custodians, with no unified routing layer connecting them today.

The businesses that solve this fragmentation through automated routing, seamless conversion, and multi-issuer acceptance are positioned to command significant premiums across a market with nearly $33 trillion in annualized transaction volume.

The Spread Mechanic: Hundreds of Issuers Are Coming:

Any firm with a scalable platform and a large user base will issue its own stablecoin and pocket the spread between the yield on T-bills and what it passes to holders. The general framework is to issue $1 of stablecoins, hold $1 of T-bills generating 4-5% yield, pass little to none of that yield to the holder, and keep the net spread as pure contribution margin. At scale, this is an extraordinarily attractive model requiring minimal incremental cost per unit.

The ultimate outcome is a predictable wave of additional stablecoin issuers. Financial institutions and payments networks will issue first, followed by big tech and consumer platforms seeking to capture more value across the payment stack. Additionally, sovereigns and central banks will also issue their own digital currencies to leverage high-speed transfers and settlement architecture. Lastly, legacy retail platforms with large and loyal customer bases will like follow-suit as the regulatory and technical infrastructure matures. Each wave of new entrants compounds the fragmentation problem and increases the value of the infrastructure that routes between them, setting up a winner-take-most dynamic among the intermediary layer.

Programmable Money & the AI Economy:

The rise of autonomous software agents introduces a new category of economic actors that require real-time access to capital. Traditional financial rails cannot support high-frequency transactions due to banking hours, compliance friction, and settlement delays. Stablecoins represent the first globally accessible settlement layer capable of supporting machine-to-machine commerce at the speed and scale that AI infrastructure needs.

Conditional Flows: Payments execute automatically when conditions are met, with no intermediaries and no delays. This enables fully automated treasury operations across complex multi-party agreements, with enforcement at the code level.

Always-On Liquidity: Settlement occurs instantly and is available 365 days a year, with no banking hours and no weekend delays. AI agents can transact and deploy capital in real time, around the clock, and autonomously, with capabilities that traditional financial rails cannot support today.

Low Issuance Costs: Any institution can issue stablecoins at a fraction of traditional product costs. Stablecoins do not require card networks or legacy clearing systems, with nearly zero marginal cost per transaction.

No KYC Requirements: Permissionless wallets enable frictionless machine-to-machine payments at scale. Stablecoins are the only viable settlement layer for AI agents that cannot complete traditional KYC flows, making them the default infrastructure for the agentic economy.

Automated Execution: Payments, escrow, and payroll, trigger on-chain with no human intervention. Code enforces pre-determined requirements without the need for legal contracts or third-party involvement.

Growth Trajectory:

Stablecoin market capitalization growth has accelerated materially since 2020. The five-year CAGR stands at 62%, with 49% year-over-year growth recorded in 2025 following the passage of the GENIUS Act, which removed the final major regulatory barriers to institutional adoption. The stablecoin market is entering a phase of infrastructure-led expansion that mirrors the early buildout of the internet payment stack.

Stablecoins as the Bridge to Bitcoin:

Every dollar deployed into stablecoin infrastructure builds the rails that all digital assets depend on. Custody solutions, on/off-ramps, compliance architecture, cross-chain bridges, and payment integrations at large fintechs like Visa, Mastercard, and Stripe, create foundational layers that onboard billions of users to what makes Bitcoin allocation possible in every part of the capital stack.

The more stablecoins succeed as programmable fiat, the more naturally they become an entry point into something harder and scarcer. Users who begin by holding a dollar token on a blockchain are taking their first steps into a world governed by cryptographic scarcity. Stablecoins are the Trojan horse that delivers the institutional credibility and global infrastructure Bitcoin needs to fulfill its role as the defining store of value for the digital age.

Where Early Riders Invests:

Early Riders focuses on the infrastructure layer that enables stablecoin adoption rather than the issuance layer itself. While hundreds of firms will launch stablecoins, the expected value will accrue to the infrastructure that allows these assets to move seamlessly across networks, issuers, and financial systems.

Stablecoin Routing Infrastructure: The middleware layer that routes payments between issuers and resolves liquidity mismatches in real time for merchants and institutions.

Enterprise Treasury & Reconciliation Tools: Software that enables businesses receiving stablecoin payments across multiple issuers and chains to reconcile, convert, and report without manual intervention.

Payment Acceptance Layers: The checkout and settlement infrastructure that allows merchants to accept any stablecoin from any network and receive settlement in their preferred currency or asset.

Institutional Settlement Infrastructure: Compliance-native and custody-integrated settlement rails that allow banks, asset managers, and fintech platforms to settle institutional volumes on stablecoin networks with full auditability.

Conclusion:

Stablecoins are evolving from niche digital assets into foundational financial infrastructure. The regulatory environment has cleared, institutional adoption is accelerating, and hundreds of new issuers are entering the market. These new issuers will each add a new layer of fragmentation that increases the value of the infrastructure that connects them. We believe the largest opportunity in this market to be the infrastructure that makes the stablecoin economy function: the routing layers, liquidity aggregators, settlement networks, and reconciliation tools that sit between issuers and the businesses and consumers who use their products.

Interested in learning more about Early Riders?

earlyriders.com