AI & The Push & Pull of Deflation & The Right Denominator

Link to the full Research in PDF

The World Used to Move Slowly

For most of human history, the world barely changed within a single lifetime. Controlling fire took hundreds of thousands of years to spread across human populations. Agriculture, first cultivated roughly 12,000 years ago in the Fertile Crescent, took millennia to reach even neighboring regions, spreading across Europe at roughly one kilometer per year. The wheel, invented around 3500 BCE in Mesopotamia, took over a thousand years to reach Egypt, only 800 miles away.

Ideas had no infrastructure to travel on. Knowledge was transmitted by word of mouth, from one person to the next, across dirt roads that barely connected neighboring villages. A farmer’s hard-won insights about crop rotation might never leave their valley, and the infrastructure to share ideas didn’t exist.

Then something changed.

Compounding Innovations

The British writer Matt Ridley coined the phrase “ideas having sex” to describe what happens when concepts from different domains collide and combine. What the data makes undeniable is that the speed of this process is a function of distribution infrastructure. The better the infrastructure for sharing ideas, the faster they combine, and the faster the next wave of innovation arrives.

The printing press, invented by Gutenberg around 1440, was the first great accelerant. Within 60 years, it had spread to over 200 European cities, producing more than 20 million volumes by 1500. But even with this leap, it took roughly 400 years for European literacy to reach 50 percent of the adult population. The press could produce books, but the supporting infrastructure of schools, roads, and a literate class to teach the next generation had to be built from scratch.

Electricity, which began its commercial life with Edison’s practical bulb in 1879, reached 50 percent of U.S. households by 1924, which took nearly 45 years. The telephone took a similar timeline. The automobile, once Ford’s assembly line made it affordable, reached 50 percent household penetration in roughly 40 years. Then globalization and the pollination of cross disciplinary ideas caused the compression to begin in earnest.

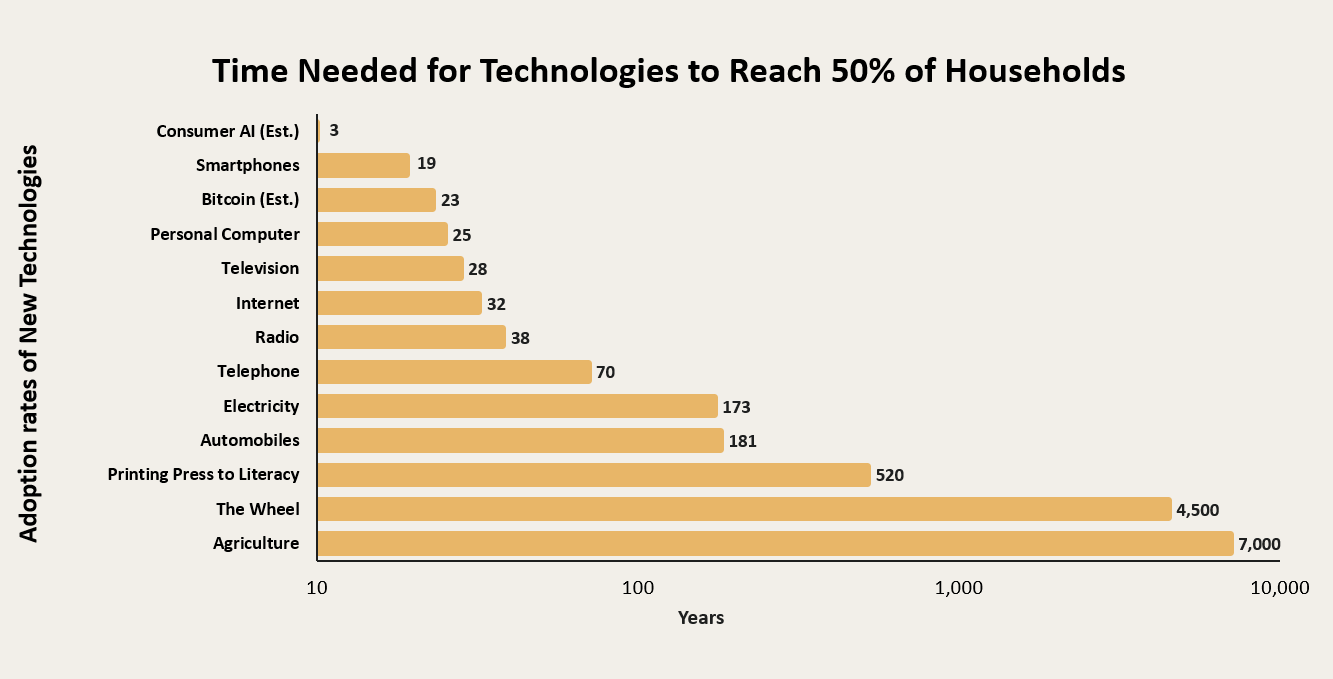

Radio hit 50 percent of American households in just 10 years. Television did it in under 5. The personal computer took 19 years, the internet took 12, and smartphones only took 6 years. Remarkably, ChatGPT reached 100 million users in only two months, and AI touched 50% of households within three years which is the fastest adoption of any technology in human history. ChatGPT was in such strong demand due to the ability to harness information across disciplines at a rate faster than ever before, compounding both knowledge and skills.

The half-life of adoption, which is the time it takes a transformative technology to reach half the population, has compressed from millennia to just a few months, and the compression is accelerating.

Why Each Wave is Faster and Larger Than the Last

There is a foundational reason each wave arrives faster than its predecessor: it rides on the rails of the previous one. The printing press needed roads and schools to teach literacy. Electricity needed an entirely new generation and distribution infrastructure, including power plants and copper wiring to every home. The telephone needed its own physical network of poles and cables.

Radio was able to leverage existing electricity infrastructure. Television leveraged radio broadcast infrastructure and electronics manufacturing. The internet leveraged the telephone network’s copper and fiber. Smartphones leveraged cellular networks, the internet, and decades of semiconductor miniaturization.

Most technological waves are growing on top of or in tandem with the infrastructure and distribution provided by other waves, driving faster adoption and more meaningful outcomes. The infrastructure for distributing the next breakthrough already exists before the breakthrough happens. AI tools did not need to build the internet, manufacture smartphones, or teach people how to use apps, and arguably could not have existed at nearly the same scale without those breakthroughs.

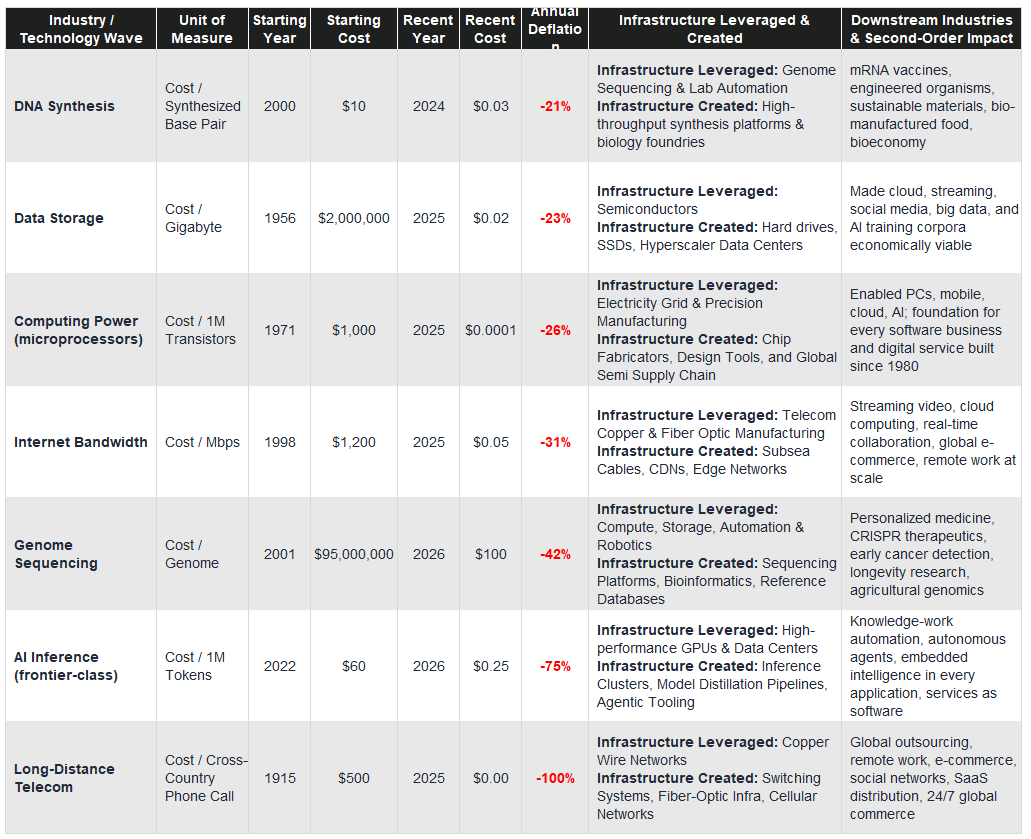

Every major technological wave does the same thing to the economy: it makes more output per unit of input, which drives the cost of goods and services down across every industry the technology touches.

These implications go well beyond technology, and directly into the foundations of the monetary system.

The Inescapable Reality of the Right Denominator

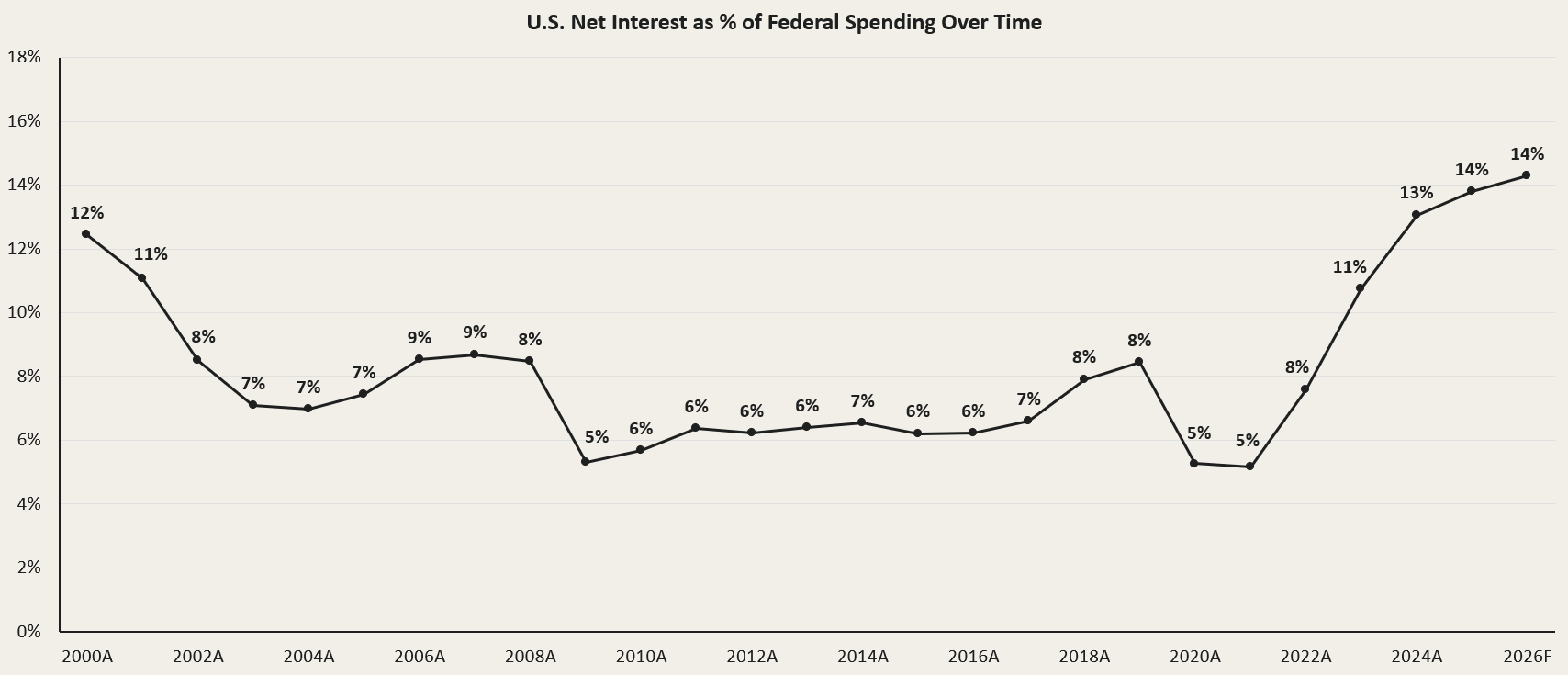

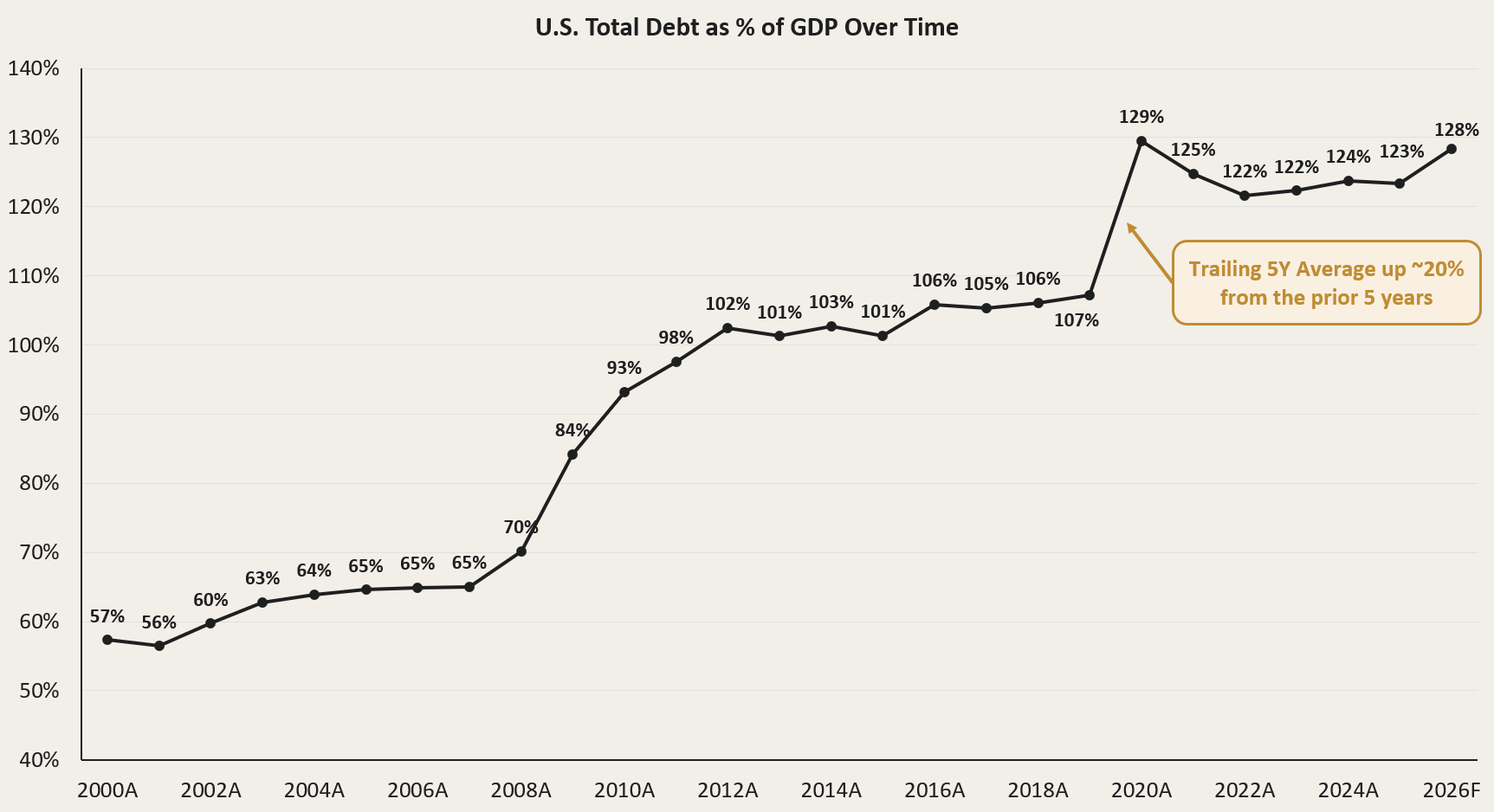

This structural reality creates an impossible problem for central banks, and for the Federal Reserve in particular. The Fed targets 2 percent inflation, while the underlying technology stack is driving 6 percent or more deflation across physical industries and services. The money supply must therefore expand by roughly 7 percent annually just to maintain the 2% consumer price index illusion. That expansion is exactly what is eroding the real value of savings accounts, pension funds, and what people believe represents their wealth. As AI accelerates deflation across manufacturing, logistics, healthcare, and professional services, each wave builds on the last and arrives faster and with a larger deflationary footprint. As a result,the fiscal response becomes inevitable. This theory has been proven with the Kabuki theatre of the Department of government efficiency. Both debt and the federal deficit will continue to grow with no appetite for structural spending cuts from congress. Interest expense consumes a growing portion of the federal budget as Treasury yields rise to compensate for inflation. The only option left for a government that will not cut spending or raise taxes sufficiently, is to inflate the debt away through currency expansion.

"We can both grow the economy and control the debt. What is important is that the economy grows faster than the debt. If we change the growth trajectory of the country, of the economy, then we will stabilize our finances and grow our way out of this." - Treasury Secretary Scott Bessent.

The U.S. fiscal position has deteriorated past 130% debt-to-GDP with no credible political path toward discipline. The debt must be continually rolled over and financed by an expanding monetary supply that dilutes the purchasing power of every dollar in circulation.

The AI driven corporate deflation has driven credit markets to increasingly reprice risk across the fixed-income spectrum, causing private credit funds to increasingly gate redemptions, highlighting counterparty risk and false economic signals.

The accelerating deflation will increasingly cause firms to be unable to pay interest on outstanding debt, and monetary authorities will respond as always by intensifying liquidity injections to prevent debt deflation spirals. As the money supply expands further and redemptions from traditional fixed-income instruments will accelerate. Additionally, real yields will turn deeply negative, and credit markets will reprice assets accordingly.

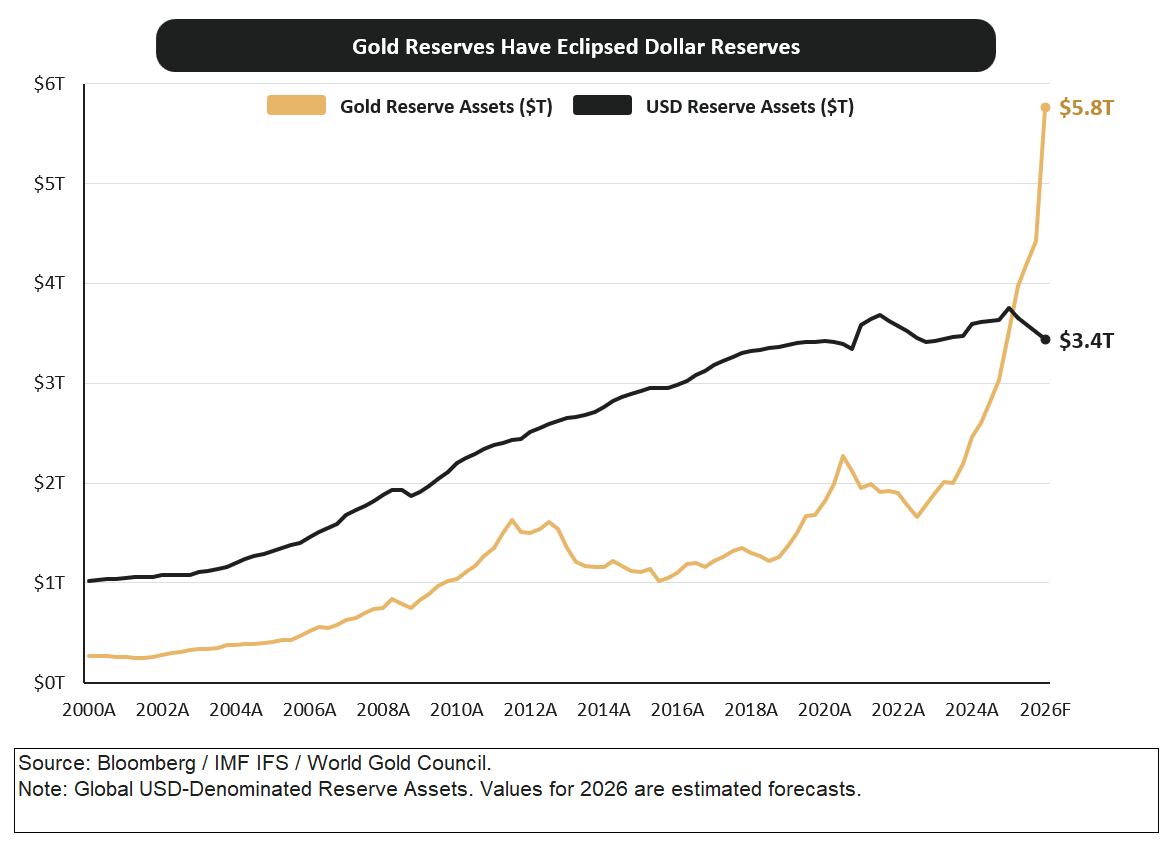

This is the deliberate policy response to technology’s structural deflation, which is designed to preserve a financial system built on the assumption that the money supply would always expand. M2 money supply growth has accelerated dramatically since 2020, driving persistent asset price inflation despite productivity gains from AI and automation, as well as a growing divergence between those who own appreciating assets and those who earn wages in a depreciating currency. Gold, which has served as scarce money for millenia and increasingly bitcoin, with its credibly scarce supply, becomes increasingly relevant as the world sees the dollar as an untenable option.

The Pull of Commodity Inflation

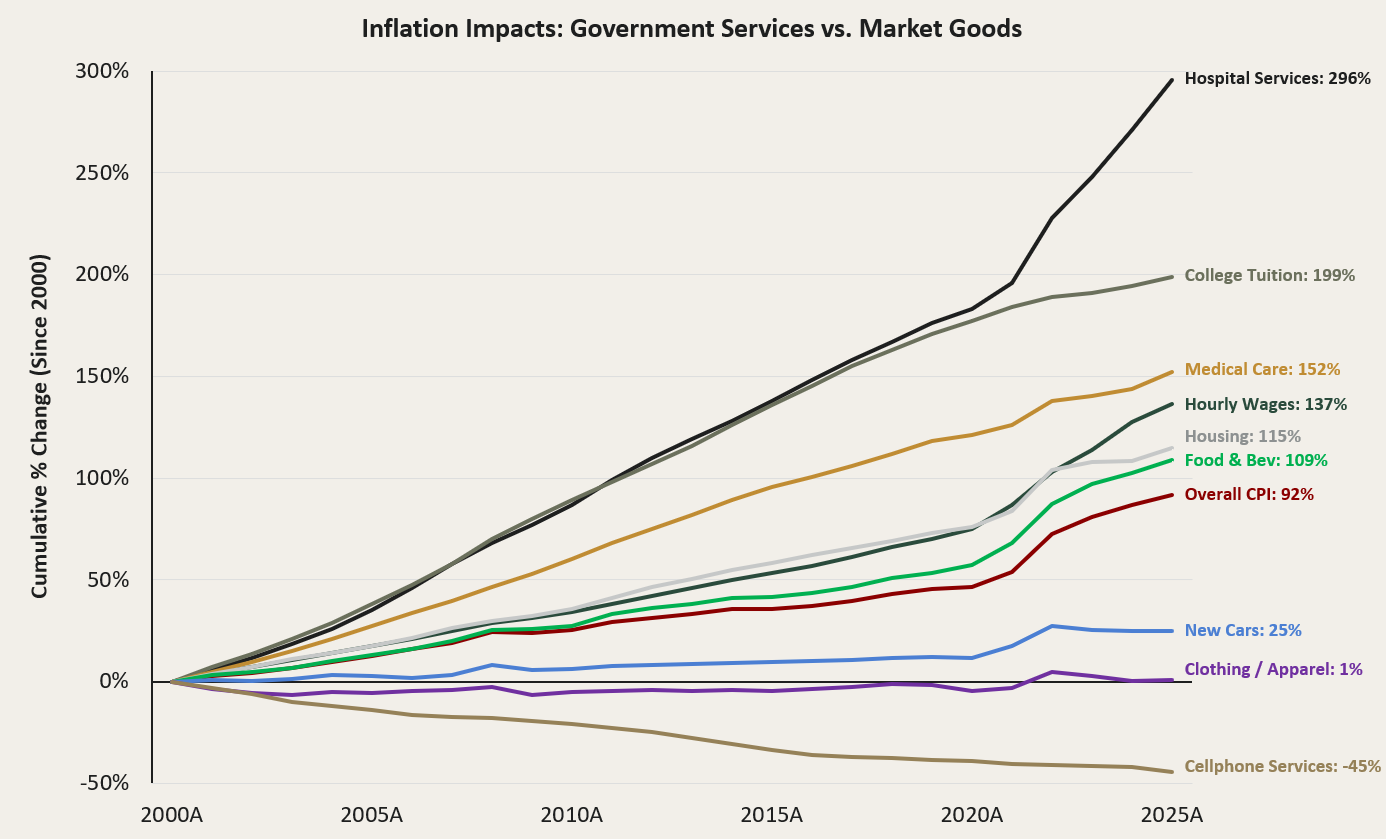

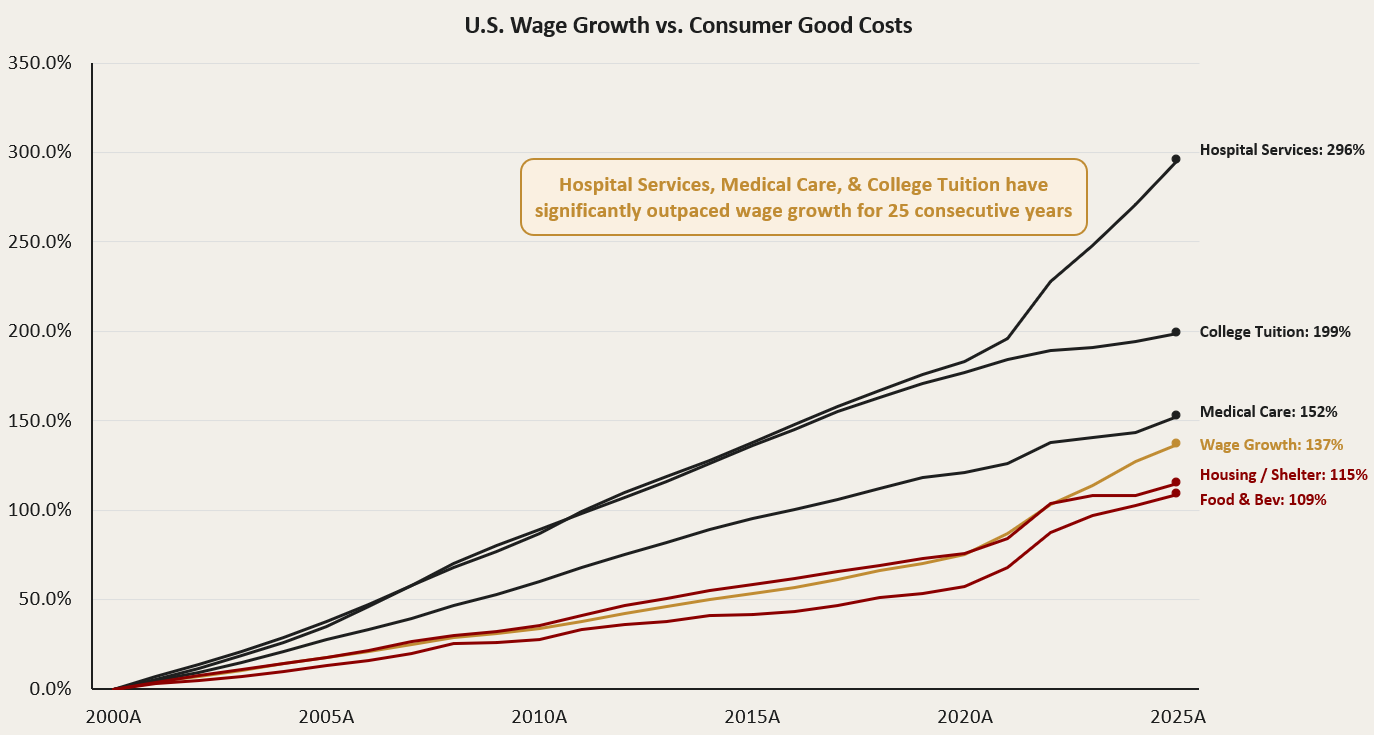

The innovation led deflation does not show up evenly across products and necessities, as most of the key inputs to everyday life have seen massive inflation, and continued to squeeze Americans. For a while the problem mostly went unnoticed as nominal balances rose, equity markets and housing prices continued to hit new highs, and the resulting wealth effect appears to benefit everyone with assets.

However, cost inflation in housing, education, and healthcare outpaces wage growth by a widening margin each year, and the living standard improvements that should flow from technological deflation, never reach the household level. This dynamic is due to those gains being inflated away at an accelerating rate, and younger generations without assets feel completely left behind by the wrong system. The technological progress continues to accelerate, but most people don’t reap the benefits with their money inflating away.

The deeper challenge is that counterparty risk has become real in a way that it has not been since Bretton Woods collapsed in 1971. The United States cannot simultaneously run massive fiscal deficits, maintain a hollowed-out manufacturing base, and provide the global security umbrella that underpins dollar hegemony. This is Triffin’s dilemma on steroids: the currency that must finance global trade is issued by a government running structural deficits with neither the political capacity nor the willingness to correct course. AI accelerates this tension by widening the gap between those with access to computational resources, capital and returns which compound through deflationary technology, and those who continue to experience inflation across crucial items, which continue to outpace wage growth.

Global Monetary Implications

The resulting wealth concentration causes political instability at home and pushes governments toward nationalist posturing and geopolitical confrontation abroad. Global supply chains fragment as trade relationships fray, and kinetic conflict accelerates the breakdown of the post-war financial order, further driving inflation across commodities. Global central banks across Asia, the Middle East, and Latin America begin diversifying out of Treasuries to increasingly avoid the U.S. counterparty and seizure risks after the seizure of Russian Treasuries by the U.S. in 2022.

The first instinct of most central banks will be to move into gold, and that instinct is already playing out. Gold is the asset central bankers understand, the one with millennia of precedent and no learning curve. Central bank gold purchases have surged to levels not seen in decades, and that trend will accelerate as dollar confidence continually erodes. Right now, bitcoin is too small for major central banks to take very meaningful stakes. However, gold and bitcoin share almost all of the same fundamental properties that make them the most attractive reserve assets. Both are scarce, both exist outside the liability structure of any single government, both serve as stores of value independent of counterparty risk, and both function as hedges against the very currency debasement central banks are being forced to participate in.

The critical difference is that bitcoin adds digital portability, borderless settlement, programmability, and divisibility that gold cannot offer. Central banks will move into bitcoin as well, though not as heavily as gold at first, because institutions move incrementally and gold provides the political cover of tradition. But the rise in gold will do something important for bitcoin: it will validate the thesis of hard money and monetary scarcity at the largest scale to a global audience. This will continue to play out as investors and institutions watch gold perform, precisely because fiat currencies are weakening. Many of these investors and institutions will recognize that bitcoin offers the same properties as gold, but in a natively digital form that is better suited to the financial infrastructure of the coming decades.

However, in regions where it is difficult and costly to transport gold, especially for settlement, countries are increasingly turning towards bitcoin. The Financial Times has reported that a spokesperson for Iran's Oil, Gas and Petrochemical Products Exporters' Union, is requesting payment in bitcoin for safe passage through the strait of Hormuz because of bitcoin’s seizure resistant properties. While we do not champion sanctions evasion, endorse the Iranian regime, or root for geopolitical conflict as a tailwind for bitcoin, it is important to observe. In the increasingly fractured world, the necessity of decentralized money with no counterparty becomes ever more important.

During the outbreak of the Russia/Ukraine war, the US seized Russian treasuries and gold, which highlighted to potentially antagonistic countries that bitcoin is a seizure resistant money.

The early movers are not taking an enormous risk; they are the ones who see the risk of not acting and are positioning accordingly. El Salvador’s adoption of bitcoin as legal tender stands as a proof of concept. There are over 11 countries mining bitcoin today using state resources. The next wave will come from sovereign wealth funds seeking uncorrelated returns, national pension systems looking to preserve purchasing power, and central bank reserve portfolios diversifying beyond Treasuries and gold.

The dollar does not need to collapse for this reallocation to accelerate; it merely needs to continue to weaken relative to real scarcity, and that will shift allocation behavior at the institutional and sovereign level. False signals in the economy, generated by monetary inflation masking technological deflation, produce false investment outcomes. Companies investing in capacity that appears profitable only because of currency expansion, find their returns compressed when the denominator catches up.

Stablecoins As A Bitcoin Accelerant

Meanwhile, the United States is actively pushing dollar-denominated stablecoins as a strategic instrument to extend the dollar’s dominance through digital rails. For the U.S. Treasury, stablecoins represent a mechanism to generate demand for Treasuries at scale: every dollar-backed stablecoin in circulation is collateralized by Treasury bills and short-duration government debt, creating a new class of buyers that grows automatically as stablecoin adoption widens. For individuals in countries with weaker local currencies, from Nigeria to Argentina to Turkey, dollar-denominated stablecoins represent something even more immediate: a better store of value than their own national money, accessible through a smartphone without needing a U.S. bank account. The result is grassroots adoption from the ground up, as hundreds of millions of people in emerging markets begin holding and transacting in digital dollars.

This adoption creates a global buildout of digital money infrastructure. Wallets, exchanges, on-ramps, off-ramps, payment processors, and trading infrastructure are being constructed at an accelerating pace across the largest banks and payment processors, with access to emerging markets. However, the rails built for digital dollars can easily be used for bitcoin with only a few minor tweaks, riding mostly the same infrastructure. As those who initially adopted stablecoins for their lack of volatility begin to experience the same inflationary pressures in housing, food, energy, and essentials,they will increasingly ask why they are holding a digital version of a currency that still loses purchasing power every year.

Bitcoin’s growing maturity and its declining volatility through market adoption, makes it an increasingly viable alternative for people who came to digital assets seeking stability and now want something that actually preserves value over time. The decentralized and borderless nature of bitcoin is not a feature people adopt because it sounds appealing in the abstract; it is a feature they adopt because it becomes necessary as their local currencies continue to inflate. The companies who build wallets, payment providers, and settlement networks for stablecoins are simultaneously building it out for bitcoin unknowingly. build infrastructure and that infrastructure expands access to bitcoin. As inflation rises, bitcoin adoption accelerates. Like past technological shifts from the printing press to the internet, each wave of infrastructure doesn’t just enable the next; it makes it inevitable.

Regulatory clarity through frameworks like the GENIUS Act and the CLARITY Act, combined with in-house institutional-grade custody from established financial firms, removes the friction that has prevented nation-state participation at scale. Once these barriers fall, bitcoin allocation transitions to a fiduciary imperative.

Smart Money Is Moving

The market is beginning to internalize scarcity in a way that has not been seen before. January 2024 saw the approval of spot bitcoin ETFs in the United States, and BlackRock's IBIT became the fastest-growing ETF ever, reaching roughly $97 billion in assets under management by early 2026. Other financial institutions know bitcoin is here to stay, causing Morgan Stanley to be the first major U.S. bank to launch a proprietary spot bitcoin ETF, listing the Morgan Stanley Bitcoin Trust (MSBT) on NYSE Arca at 0.14%. Morgan Stanley’s spot bitcoin ETF is now the lowest fee on the market and is 11 bps below IBIT. With roughly 16,000 Morgan Stanley financial advisors overseeing $6.2 trillion in client assets now equipped to distribute a bitcoin product carrying the bank's own name, the distribution infrastructure for bitcoin has shifted from fintech-native issuers to the heart of traditional Wall Street. Bitcoin is now accessible within existing institutional frameworks; it can be held in tax-advantaged accounts, included in diversified portfolios, and traded through the same prime brokerage relationships where institutions already operate. Other institutions will follow because the competition and incentives drive it.

With 21 million fixed supply and growing institutional demand, every new wave of capital compresses the float and pushes the price higher. Early movers structurally outperform not because of luck, but because they recognized the denominator problem first and acted when prices reflected only early adoption. They increasingly recognize bitcoin is a repricing of monetary premium from infinite supply, where central banks can always print more, to fixed supply, where scarcity is enforced by mathematics.

The first to recognize this were individuals operating as a consensus of one: early bitcoin holders, family offices, and high-net-worth investors who understood that M2 expansion is itself a risk position and that holding wealth in a system designed to inflate is a losing trade. They have already been rewarded, as purchasing power has dramatically outpaced what dollar savers achieved over the same period. That visible outperformance pulls in the next wave: large institutional allocators, endowments, and pension funds that cannot ignore returns outpacing their benchmarks. Infrastructure unlocks adoption, following the same pattern from Part I: each wave of infrastructure makes the next wave possible, and the stablecoin-driven buildout of global digital money infrastructure is accelerating this cycle faster than any previous wave.

The divide this transition creates is structural and will compound over decades. Those who choose the right denominator will find their wealth reflects the real productivity gains created by AI. Purchasing power denominated in bitcoin will rise as technology creates deflation in goods and services, allowing holders to capture the revolution in the form of increasing real wealth. Those who remain in the wrong denominator, will watch nominal wealth grow on paper, while real purchasing power erodes beneath them. This is a structural divergence that compounds over time, much like that of the 1970s gold transition. However,this transition is faster, more global, and digitally native, moving at network speed rather than the pace of institutional bureaucracy.

There is a powerful convergence taking shape where AI meets bitcoin, and understanding it is essential to seeing where capital will flow over the next decade. AI and deflation follow the same concepts from Moore’s Law: costs per unit of computation fall exponentially as efficiency improvements compound across hardware and software. Bitcoin follows Metcalfe’s Law: value increases with the square of participants and nodes, creating exponential appreciation as adoption widens. When these two exponential forces converge, the result is multiplicative. Companies building with AI while understanding the scarcity dynamics of computational resources and fixed-supply assets will naturally gravitate toward bitcoin as the definitive settlement and value storage layer. On the flip side, companies whose core competency is AI will develop better tooling and intuition for understanding technological scarcity, and will naturally recognize why a fixed-supply asset matters more than an inflationary one. Technology companies are already adopting bitcoin as a strategic treasury anchor, recognizing that a finite and scarce asset appreciates in real terms as they build stronger products, while the dollars they would otherwise hold, depreciate at a growing rate through M2 expansion. Agents will be more efficient and secure when transacting in money, and in order to do so need to have money which is native and transportable over the internet.

At the same time, a new generation of companies is being built with the goal of more bitcoin as their north star. The companies that understand both the technology scarcity thesis from AI and the ability to save earned money in scarce digital assets will be the category winners. This is the infrastructure opportunity at the intersection of AI and bitcoin: companies designed to operate in a world where value is measured in scarce assets, where trust is replaced by mathematical proof, and where the financial system is being reconstructed with bitcoin at its core scarcity aspect.

Early Riders is investing with this view of how the world will play out, backing the founders who understand the correct opportunity costs. The winners of the past and next decades have increasingly moved from dollars to bitcoin over the past decade because the technology stack is structurally deflationary, while the monetary response will be persistently inflationary. The transition from infinite supply to scarce digital assets creates an enormous infrastructure opportunity: custody solutions that make bitcoin as safe as traditional finance made dollars, lenders allowing for safe and secure credit, and on-ramps and off-ramps that connect legacy finance to bitcoin-native systems.

The full-stack financial system will be rebuilt over the next few decades with bitcoin at its core because it is the only asset that solves the denominator problem when everything else is being inflated away. We look for businesses that have bitcoin built into their founding team’s worldview and that treat it as a core strategic anchor and use the technological waves to help them do more with less. These companies will be the category winners because they understand both the technology scarcity thesis from AI and the infrastructure opportunity from building a system where value is measured in scarce assets.

The world is waking up to a reality that was, until recently, only visible to those watching the denominator carefully: the monetary system is broken because it cannot simultaneously provide the stability savers require and the inflationary response governments need to manage decades of fiscal expansion. Bitcoin solves this by removing the discretionary human element entirely. Fixed supply, transparent rules, and global accessibility mean the denominator cannot be manipulated by committees, corrupted by politics, or expanded to finance the promises of arbitrary government entities. The transition from measuring wealth in dollars to measuring it in bitcoin is already underway, visible in institutional adoption, sovereign interest, and the purchasing power trajectories of those who made the shift. Early Riders exists to find and back the founders building the infrastructure that makes this transition inevitable.

To learn more, the full article is available here:

Early Riders is the first bitcoin-denominated venture firm, raising, holding, investing, and returning capital in bitcoin. Learn more about how to get involved www.earlyriders.com.

Make sure to keep up with all our research at earlyriders.com/research.