Early Riders | Open Range Weekly | 05.03.26

Bitcoin was up ~1% this week to a market capitalization of $1.57T.

Early Riders Media

This week’s podcast, saw institutional pressure mount to freeze Satoshi’s coins, which echoed the original Block Size Wars and raised new questions about who controls Bitcoin’s future. The discussion also covered Treasury Secretary Bessent’s $344 million Tether freeze tied to Iran, DeFi’s decentralization theater after the KelpDAO and Aave exploit, and new data showing that the total headcount included in the S&P 500 fell by 400,000 jobs in 2025.

You can find all our episodes on our podcast website as well as listen on YouTube, Apple, and Spotify.

Industry & Institutional Updates

Tether proposed merging Twenty One Capital with Strike and Elektron Energy, to create an integrated public bitcoin platform spanning treasury, mining, financial services, lending, and capital markets.

Tether launched modular bitcoin mining infrastructure with Canaan and ACME Swisstech, separating compute, power, and cooling components into independently upgradeable systems.

Lightspark introduced Grid Global Accounts to offer platforms dollar accounts, Visa cards, instant payouts, bitcoin support, and AI agent payment permissions through one integration.

Block disclosed $2.2B in bitcoin holdings across customer balances and corporate treasury as part of a new transparency push.

Strategy purchased an additional 3,273 bitcoin totaling nearly $255M as it continues to increase its ongoing treasury holdings.

Block launched a new Bitkey hardware wallet with secure screen, automatic bitcoin earning and 5% bitcoin back rewards inside Cash App, proof of reserves covering $2.2B, and an NFC tap-to-pay demo for Square merchants that settles over the lightning network.

Aven launched a Bitcoin-backed Visa card that lets users access credit against bitcoin collateral without selling their holdings.

Lightspark and Visa partnered to support stablecoin and Bitcoin-linked debit card issuance across more than 100 countries.

Meta began rolling out USDC payouts for creators through Stripe, marking its return to stablecoin-enabled payments.

Anchorage Digital and M0 partnered to provide regulated issuance and modular infrastructure for companies building stablecoins.

OKX introduced Agent Payments Protocol, an open standard for AI agents to settle transactions autonomously.

Stable Sea partnered with WisdomTree to bring tokenized treasury access into business cash management workflows.

Gemini launched agentic trading tools that allow users to connect AI models like Claude and ChatGPT to automate digital asset trading.

PayPal restructured into three standalone business segments under new CEO Enrique Lores, elevating Venmo to its own reporting unit for the first time and potentially positioning it for sale.

Visa expanded its stablecoin settlement pilot across five additional blockchains as its annualized stablecoin settlement run-rate reached $7B.

Tether led a $14 million Series A for Argentine crypto wallet Belo, which serves over 3 million Latin American users and plans to expand stablecoin payment infrastructure into multiple Latin American countries.

Regulatory & Sovereign Updates

The U.S. Treasury seized $500M in Iranian-linked digital assets as sanctions enforcement increasingly reaches onchain.

North Korean hackers accounted for 76% of 2026's digital asset losses through April, according to TRM Labs.

Canadian Regulators announced plans to ban crypto ATMs over fraud and money laundering concerns.

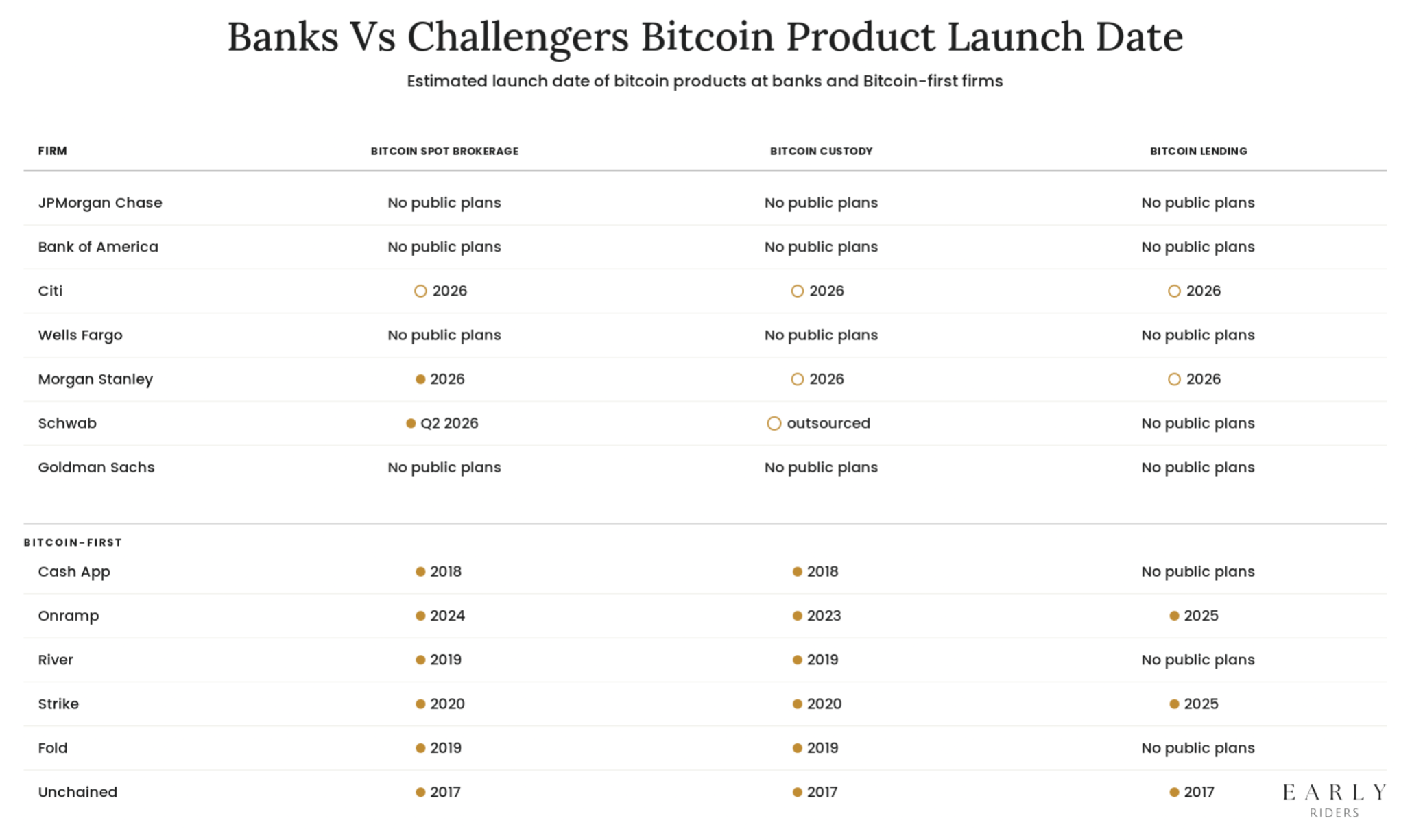

What We're Watching: The Bitcoin-Banking Merger is Here, and the Banks are Losing

Banks are finally marketing and signaling plans for bitcoin products after years of clients asking and assets leaving bank platforms to find bitcoin. Broader adoption is the welcome consequence, but the products themselves remain suboptimal. Morgan Stanley, Schwab, Goldman, and others have launched their initial digital asset products by assembling infrastructure built by other firms. Paxos custodies Schwab's client Bitcoin, and Coinbase handles most of the bank-affiliated ETFs until the in-house custody builds reach completion. Each of these launches is an acknowledgment that the issuing bank does not yet possess the capability to deliver the product on its own infrastructure.

The outsourcing problem would be less consequential if these same institutions were at least competing effectively on the traditional side of the client relationship, which is not currently the case. The banks are paying third parties to build their digital asset franchises are simultaneously paying close to zero interest on client cash balances, while Bitcoin-first firms have begun offering up to 5% on dollar balances, card rewards on spending, and integrated dollar-Bitcoin accounts within a single product surface. Bitcoin-driven asset outflow has been a fact of bank platform economics for several years, and the GENIUS Act, which brings stablecoins into a clearer regulatory perimeter, combined with the current administration's broader posture toward digital assets, now extends that outflow to the dollar side of the relationship as well.

How the Banks are Showing Up

Every issuer of a spot Bitcoin ETF in 2024 was a pure-play asset manager, which is no longer true of the competitive set. What has remained constant is that every major bank entry into the digital asset stack has depended on third-party infrastructure, given that none of the bank-affiliated issuers has shipped a fully in-house digital asset product as of this writing.

Morgan Stanley has committed to building Bitcoin custody and trade execution in-house, which is the most serious of the three approaches observed among the large incumbents and also the one most consistent with the scale of the franchise it is protecting, namely roughly $8 trillion in client-advised assets, approximately 16,000 financial advisors, and a formal 0-4% Bitcoin allocation recommendation that had previously been serviced through third-party products such as iBit and FBTC. The firm launched its own ETF earlier this month at the low end of the industry fee band to take share from the earlier dominant issuers. The custody is outsourced to Coinbase, which leaves the long-run economics of the asset relationship with the sub-custodian rather than with the bank. The firm plans to build custody and trading services in house, but the quickest way to go to market is through partnerships.

The build itself is slow, human-capital intensive, and operationally difficult for large, complex, and bureaucratic firms. In the interim, Morgan Stanley is relying on third-party sub-custodians to operate the business, with the consequence that even the most serious of the bank responses is, at present, a duct-taped version of what the firm eventually intends to own and control.

Citi is the only other major bank pursuing the same path, having committed to building digital asset custody, trade execution, and settlement infrastructure in-house rather than outsourcing to a third-party provider. The two are converging on the same conclusion for roughly the same reason, namely that owning the infrastructure is the only configuration in which the long-run client economics of the digital asset franchise accrue to the bank rather than to the firms whose rails the bank is renting. Everything about the in-house build is harder, slower, and more expensive than the alternative, which is precisely why the list of banks actually doing it is two names long.

Charles Schwab, which is structured as a brokerage holding company with a bank subsidiary rather than as a traditional commercial bank and is therefore competing from a somewhat different starting position, sits further along the same spectrum in the opposite direction, having launched spot Bitcoin and Ethereum trading with Paxos as sub-custodian at 75 basis points. At the product layer the offering looks similar to what Morgan Stanley and Citi will eventually build in-house, though underneath the surface it is structurally different, given that Schwab does not own the custody, does not own the long-run client economics of the asset custody and trade relationship, and will therefore have limited ability to extend that relationship into adjacent digital asset services. The trade-off purchases speed to market and lowers short-term reputational exposure, at the cost of leaving the core of Schwab's digital asset franchise running on infrastructure the firm did not build and does not control.

Goldman Sachs has taken a third path with a premium income Bitcoin ETF structured as an options-based yield overlay rather than as a straight spot product, which allows Goldman to charge a higher management fee than the 14 to 25 basis point band into which spot products have converged. It is also a narrower bet, because the firm is pricing for margin on a novel wrapper rather than positioning itself to capture the underlying relationship with long-term bitcoin investors

Four firms have produced three versions of the same underlying story, in which Morgan Stanley and Citi are building the native capability at a pace the category will likely reward, Schwab is renting the infrastructure from a firm that does own it, and Goldman is pricing a wrapper rather than competing for the underlying relationship at all. None of the four has the full native stack today, and all of them are, to varying degrees, stitching together infrastructure built by other firms. Over the three-to-five-year window during which the digital asset franchise is being established, the gap between the banks and the firms on which they currently depend is more likely to widen in favor of the latter than to close.

The Banks are not even Winning on Banking

The duct-taping problem on the digital asset side would matter considerably less if the banks were still winning clearly on the traditional banking side of the relationship. The product that banks actually sell to their customers, before any digital asset overlay is considered, is a set of deposit accounts that pay close to nothing on cash at a moment when short-duration treasuries and money market funds offer similar risk profiles. The average bank deposit in 2026 offers near zero yield and is deeply negative when considering inflation. Customers now have credible alternatives to leaving their working capital in an account that pays zero.

Bitcoin-first firms who have built client trust and relationships over the years through bitcoin products are now competing for the dollar side of the relationship on terms the banks have declined to match for forty years.

CashApp - Operated by Block, grew from peer-to-peer payments into the largest consumer-facing Bitcoin on-ramp in the United States and now runs a nearly complete retail banking stack: paycheck direct deposit, a debit card with cash-back on spending, a yield-paying savings product, stock and Bitcoin buying from a single balance, and Lightning-powered send and receive.

Onramp Bitcoin - Offers up to 5% earn on cash balances and 1.5% card rewards on spending, integrated with a Bitcoin brokerage, multi-institution custody, Bitcoin-collateralized lending, IRAs, and direct gold custody with the Royal Canadian Mint.

River - Through its partnership with Lead Bank, pays up to 3.3% dollar earnings routed directly into Bitcoin and places bill-pay functionality alongside its Bitcoin accumulation product.

Strike - Extended its Bitcoin-buying flagship into paycheck direct deposit, direct bill pay, and Bitcoin-collateralized lending, while operating a global payments layer that routes dollar transfers over the Lightning Network at meaningfully lower cost than the correspondent banking system.

Fold - Extended a Bitcoin rewards debit card into a full spending product that pays sats back on everyday purchases and accepts direct deposit, letting a customer route a paycheck into a single account that earns Bitcoin on every swipe. The structural economics resemble airline miles, with Bitcoin as the accrual asset rather than a loyalty point issued by the merchant.

Unchained - Operates a collaborative-custody and private-client franchise for allocators holding Bitcoin at scale, offering Bitcoin-backed loans, inherited and trust custody structures, IRAs, and a trading desk.

These firms are not competing on the dollar side by running cleverer risk models but banks have not historically felt institutional pressure to pass yield through to customers. Meanwhile the Bitcoin-first firms have built their entire franchise around building better products for customers rather than as working capital to be captured and spread-mined.

The convergence thesis has expanded beyond digital assets and now encompasses a broader repricing of the bank-client relationship, within which the Bitcoin-first firms are offering a demonstrably better deal on dollars alongside the Bitcoin-first services the banks cannot yet build. That combination is considerably harder for the banks to respond to than crypto exposure alone would have been.

The Innovator's Dilemma Applied to Banking

Christensen's theory of disruptive innovation is the most useful lens here. Incumbents usually see the disruption coming, but the same processes and values that made them successful also prevent them from adapting to it.

The banks that dominate private wealth, brokerage, and custody earned those positions by optimizing for regulatory compliance, operational reliability at scale, and spread-based monetization of client cash. Those are the right muscles for the business they already run. A digital asset franchise needs different ones. Products iterate in weeks, consumer expectations are set outside the regulated perimeter, and the pressure to pass yield through to customers is exactly what the bank operating system is built not to absorb.

Three Constraints Make this Concrete

First, absorptive capacity. A firm's ability to commercialize new external knowledge depends on the knowledge it has already built up in the area. None of the major bank-affiliated issuers has ever shipped a digital asset product. Bitcoin ETFs are the trivial case, since they slot into existing rails and get outsourced to Coinbase anyway. Custody, Bitcoin-collateralized lending, and stablecoin payments are different problems, and the product instincts needed to solve them have accumulated almost entirely outside the banks now trying to enter the category. The likely consequence is that banks will underwrite Bitcoin-collateralized lending using the balance-sheet assumptions of traditional banking and repeat the rehypothecation mistakes that blew up BlockFi, Celsius, and Genesis.

Second, operating cadence. Committee structures, compliance reviews, and procurement cycles at large banks run on timelines measured in quarters and years, while the firms they are competing against iterate in weeks. This does not dissolve because the firm has recently started caring about digital assets.

Third, human capital. The people who build this infrastructure are pioneers who do not want to manage bureaucracy, office politics, and slow-moving firms. Large banks have not been able to replicate the cultural environment that produced them. Even when they hire the right talent, they deploy it against the wrong products, putting budget into prediction markets, long-tail token listings, and tokenized wrappers rather than core custody, trade, lending, and payments.

The banks that clearly see the opportunity will struggle to execute at the pace the category demands. The banks that have not yet seen it, which is most of them, will not close the gap through internal build.

Regulation as a Timing Variable

Regulation is the principal reason the banks still have a runway at all. Under the current Basel III capital requirements, a bank holding spot Bitcoin on its balance sheet is required to reserve dollar-for-dollar against the position. That breaks the economics. Banks run on leverage, and a 100 percent capital charge on Bitcoin strips the leverage out, leaving the position to earn its way through price appreciation or thin lending yields, neither of which clears the 10 to 15 percent cost of equity a large bank is underwriting to. Non-bank competitors do not face the same treatment and therefore operate with a structural cost-of-capital advantage the banks cannot close through better execution. That is also why even Morgan Stanley's planned custody build will not translate into meaningful balance-sheet Bitcoin exposure in the near term. Citi and other large banks are reportedly lobbying to amend the treatment.

The Basel III capital treatment of crypto assets is, for that reason, likely the single most consequential regulatory variable over the next eighteen months. A favorable change would accelerate the convergence, validate the banks that are building custody now, and compress the window during which digital-first firms can operate without serious incumbent competition, whereas an unfavorable change, or more realistically a continued delay, would extend the runway for those same firms to consolidate before the banks can show up at scale. Either path buys time for one side or the other without resolving the underlying competitive asymmetry, which is that the Bitcoin-first firms are currently beating the banks on both sides of the product relationship.

The Coming End State

The banks cannot build their way out of the problem in the window available, which leaves acquisition as the only route by which they end up owning a digital asset franchise at all. The relevant firms are already visible, namely those shipping the full stack with durable customer trust and conservative product architectures. Over the next five years, some of them will be acquired at multiples the banks will later describe as expensive, and others will remain independent long enough to operate as the next generation of private banks. The banks that move early and at reasonable prices will preserve the client relationship, while others will become less relevant over time.

Regardless of how the competitive chips fall, the end customer wins either way, with better products, meaningful yield on dollars, and an integrated Bitcoin-dollar experience the industry has not previously delivered.

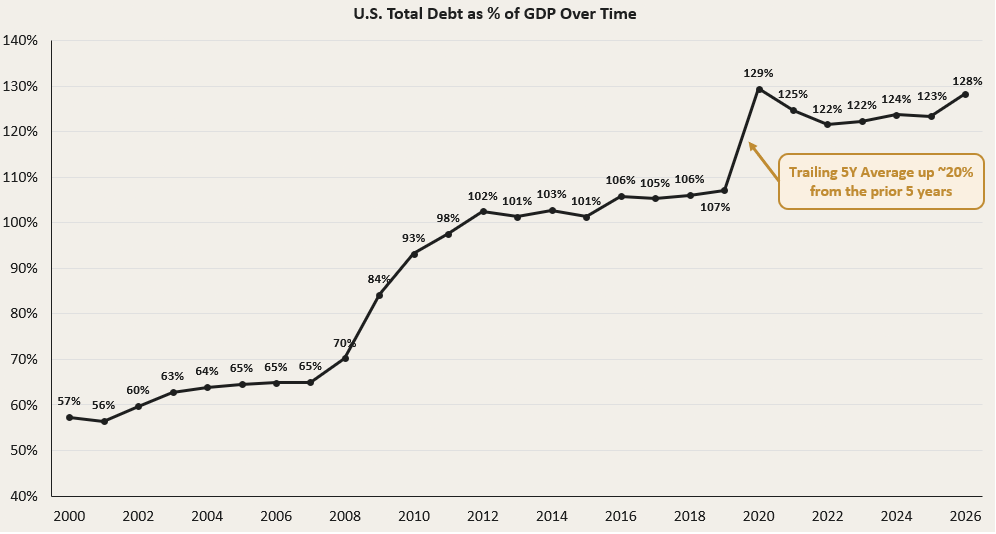

Chart of the Week

U.S. total debt as a percentage of GDP has risen from ~57% in 2000 to ~128% in 2026, with the U.S. economy now carrying more than twice as much debt relative to its output as it did at the start of the century. The key signal is the persistence: debt-to-GDP has remained above 120% since 2021, and the trailing five-year average is up ~20% from the prior five-year period, reinforcing why investors are increasingly focused on scarce assets that cannot be diluted by fiscal expansion.

Early Riders is the first bitcoin-denominated venture firm, raising, holding, investing, and returning capital in bitcoin. Learn more about how to get involved www.earlyriders.com.

Make sure to keep up with all our research at earlyriders.com/research.