Early Riders | Open Range Weekly | 03.29.26

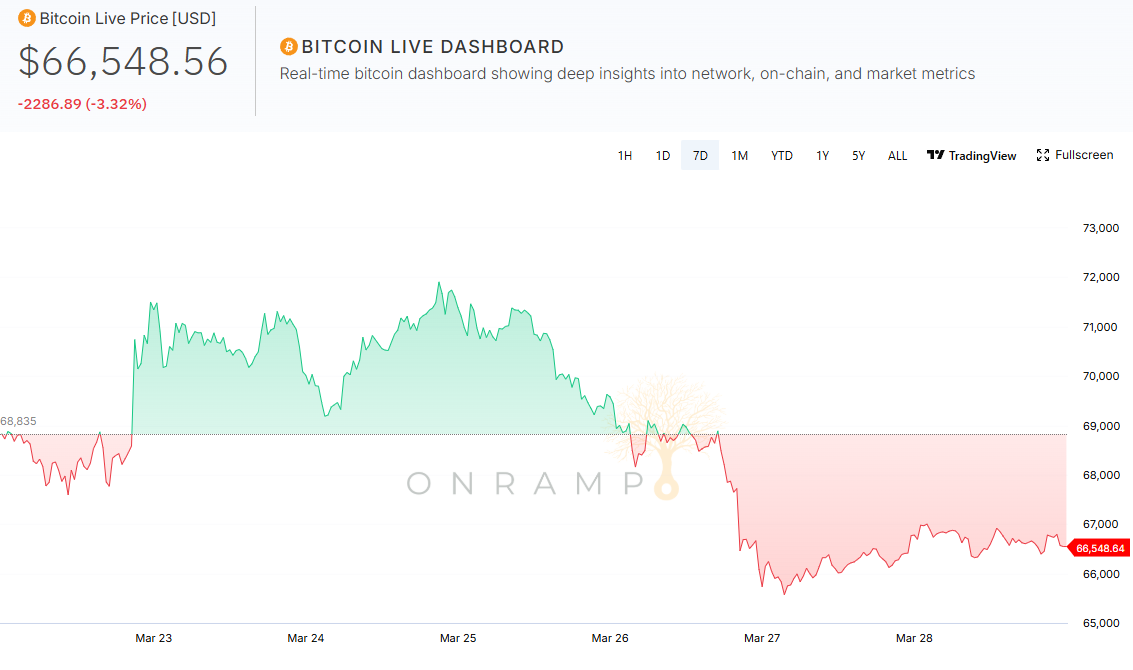

Bitcoin was down (3.3%) this week to a market capitalization of $1.33T.

Early Riders Media

On this week's podcast, Brian, Michael, and Liam navigate a volatile macro backdrop and discuss the regulatory clarity from both the CFTC and SEC on crypto securities classifications as they examine how traditional financial infrastructure is rapidly converging with bitcoin and digital asset rails.

You can find all our episodes on our podcast website as well as listen on YouTube, Apple, and Spotify.

Industry & Institutional Updates

Morgan Stanley filed a 0.14% fee for its spot Bitcoin ETF, undercutting BlackRock's IBIT at 0.25% to become the lowest-cost Bitcoin ETF on the market.

Coinbase powered the first crypto-backed conforming mortgages, letting borrowers pledge bitcoin or USDC as collateral for Fannie Mae-eligible loans.

Strategy unveiled a $44 billion equity issuance plan to fund bitcoin accumulation as holdings reached 762,099 BTC.

Core Scientific expanded its credit facility to $1 billion with a new $500 million commitment from J.P. Morgan.

BitGo reported $16.2 billion in full-year 2025 revenue, up 424% year-over-year, in its first earnings since its January NYSE IPO.

MARA Holdings sold bitcoin $1.1m in bitcoin reserves to cut convertible debt by 30%, funding a pivot toward AI and high performance computing.

Crypto.com cut 12% of its workforce, citing AI integration as making a smaller team capable of doing more.

Tether signed a Big Four accounting firm for its first-ever full independent audit, covering $184 billion in USDT circulation.

GameStop moved 4,709 bitcoin to Coinbase in order to execute a covered call strategy on the asset.

Regulatory Updates

North Carolina lawmakers introduced Senate Bill 327, proposing allocations of up to 10% of state public funds to bitcoin.

Congress released Clarity Act language prohibiting yield on stablecoin balances, immediately sending Circle stock down 20%.

What We're Watching: BitGo’s Q4 & Full Year 2025 Earnings Takeaway

BitGo reported Q4 revenue of $6.16 billion (up 440% y/y) and full-year 2025 revenue of $16.15 billion (up 424% y/y), beating consensus estimates on both the top line and EPS. Despite the beat, the stock sold off roughly 12.5% to ~$7.96. The headlines captured a $50 million net loss in Q4, driven almost entirely by unrealized mark-to-market losses on BitGo’s Bitcoin treasury as prices pulled back in late 2025, although adjusted EBITDA came in at $12.1m in 4Q25, nearly triple the $4.2m in 4Q24.

Bitgo’s adjusted EBITDA went from $3.2 million in FY24 to $32.4 million in FY25, primarily driven by the higher-quality revenue lines: subscriptions and services revenue (the most SaaS-like, highest-margin line) grew 57% to $121.5 million; staking take rates improved from 8.8% to 10.5%, reflecting better pricing power even as staking volume declined; and Stablecoin-as-a-Service contributed $66.7 million on approximately $2.2 billion in AUC. The client base doubled, growing 103.5% year-over-year to 5,322 clients and 1.2 million users, with 50% using three or more products.

However, digital asset sales, essentially BitGo's OTC desk, which represented the vast majority of FY25 revenue at $15.6B, were up over 5x y/y but gross margins declined to 0.21% from 0.47% a year ago. Notably, the sheer volume growth means gross profit dollars on this line nearly tripled y/y, from roughly $12M to $33M, but raised concerns about further unit compression as trading commoditizes further as OTC desks and prime brokers scale up.

Total assets on the platform declined 9.2% y/y to $81.6B, while staked assets were cut roughly in half to $15.6B, both reflecting the softer digital asset price environment in late 2025. Management guided Q1 2026 revenue lower sequentially, citing a decline in development fees and staking fees expected to be "significantly lower" versus Q1 2025. On valuation, $32M in adjusted EBITDA against an approximately $2B market cap implies a multiple north of 60x, requiring investors to underwrite meaningful growth from here. As a January 2026 IPO with limited float and a still-forming shareholder base, BTGO also faces the structural volatility typical of recently listed digital asset names, with lock-up overhang from pre-IPO holders adding additional near-term pressure.

The most consequential strategic development is BitGo's OCC approval to operate as a federally chartered digital asset trust bank, making it the first publicly traded company to achieve this designation. For institutional allocators (pension funds, endowments, RIAs), the regulatory credentialing required to custody digital assets is non-trivial, and a federal charter provides a level of regulatory clarity that state-level trust charters and offshore structures cannot replicate. As institutional adoption of digital assets broadens, the addressable pool of capital requiring federally regulated custody infrastructure will grow, positioning BitGo as a primary beneficiary, while sell side analysts noted BitGo's custody-oriented model may prove more resilient than transaction-dependent exchanges in a softer market, a framing we find compelling.

BitGo launched its derivatives business on January 1, 2026, processing approximately $3B in notional volume and over $3M in revenue to date. While still early, management pointed to a counter-cyclical dynamic where declining spot volumes are driving increased client demand for derivatives as hedging and yield generation tools. Stablecoin-as-a-Service AUM exceeded $5B during Q1, up from $2.8B in Q4, and the announcement of support for SoFi's stablecoin (SoFiUSD) makes BitGo the first platform to support two of the world's leading stablecoins. The lending business is also scaling and partially offsetting the softer Q1 guidance on other lines.

Going forward, the highest-priority metric is whether subscriptions and services can sustain 50%+ growth, as this remains the best proxy for platform value and the highest-margin line in the mix. On the newer initiatives, Stablecoin-as-a-Service AUM crossing $5B is encouraging, but the market will want to see that translating into durable fee revenue rather than just an AUM headline. Similarly, the derivatives business needs to demonstrate it can scale beyond its early $3M revenue run rate, especially if it is going to serve as the counter-cyclical offset to softer spot volumes amid potentially weaker digital asset prices.

Chart of the Week

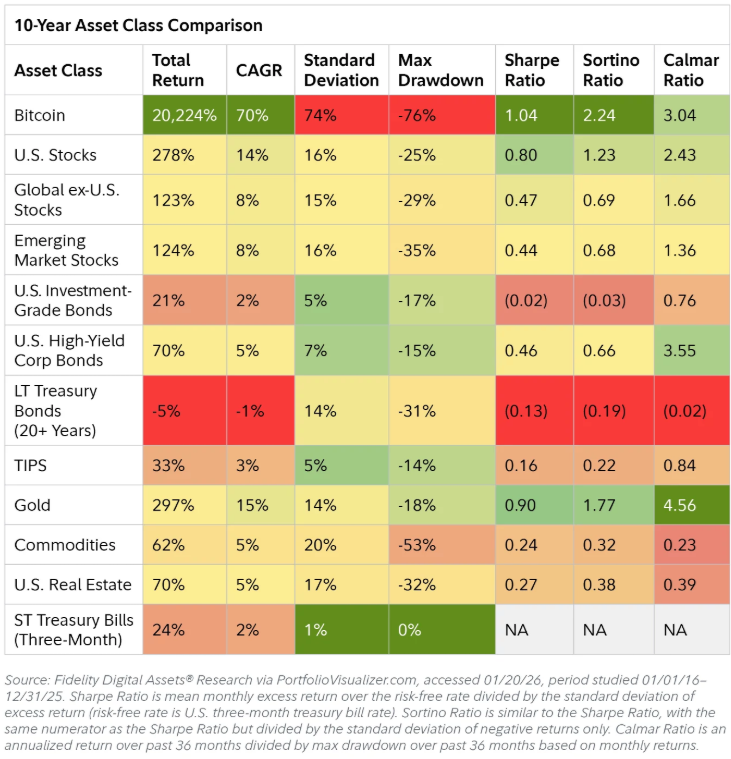

Fidelity revealed that bitcoin beats every major asset class across 4 of the 7 listed categories as the asset has generated the highest total return, CAGR, Sharpe Ratio, and Sortino Ratio over the last decade. Bitcoin has both the highest total return, but also the highest max drawdown, emphasizing the risk-on nature of the asset. Gold posted the highest Calmar ratio of any asset, delivering a 297% return over 10 years with only an -18% max drawdown.

Find this valuable? Please forward this to someone in your network who may find benefit from the information.

Early Riders is the first bitcoin-denominated venture firm, raising, holding, investing, and returning capital in bitcoin. Learn more about how to get involved www.earlyriders.com.

Make sure to keep up with all our research at earlyriders.com/research.